Thoughts on the FED/Inflation

2:43: Here are some more thoughts on the Fed/inflation.

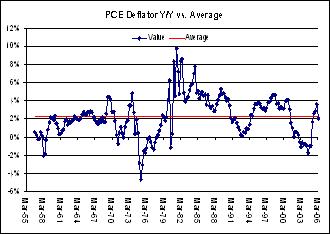

From a global perspective, the Fed has done a lot of heavy lifting. Based on the core US CPI, the fed funds rate is in neutral to restrictive territory. Historically, the fed funds rate has traded 200 bps over the core CPI. It is currently about 250 bps over and likely to go to 275 bps. Core CPI could drift higher due to the rent component. This is one problem for steady policy and a 25 bps rate hike. CPI based inflation will put downward pressure on the real funds rate in the coming months. Looking longer term at the PCE deflator, the fed funds rate has averaged 225 bps over the PCE deflator (using GDP data). The current spread is about in line with history due to an up tick in inflation in Q1. Year ago comps were very easy in part helped by aggressive discounting in autos last year. This could act to keep upward pressure on inflation and downward pressure on the real yield.

The graphic displays the extreme monetary ease of the early 2000’s. Policy tends to get restrictive when the real fed funds rate moves abut 4% over the PCE deflator. According to the graphic, policy has actually gotten looser in recent months. Note that average real funds rate was lifted by the strength of the early 1980’s. Real rates trended much lower in the 1960’s by comparison.

posted by CODACap at

8:14 AM

![]()

0 Comments:

Post a Comment

<< Home